Variable annuities are a popular financial product that allow investors to realize tax-deferred returns which convert into a stable annuity after retirement. With a guaranteed minimum death benefit, if an investor dies before retirement and their investment account is below the guaranteed level, the issuing insurer must make up the difference. From the perspective of the insurer, the risk looks like selling an equity put option that is conditioned on mortality.

The insurer has two risk management challenges: ongoing dynamic hedging of the equity and rate risk they take on through variable annuity issuance; and maintaining a reserve against adverse outcomes. These two problems are linked—insurers may be able to realize a smaller reserve if their reserve calculation incorporates a rules-based hedging strategy.

Reserve calculations using traditional risk neutral hedge methods can be computationally very expensive. The reserve calculation itself requires a Monte Carlo simulation of future equity and interest rate market moves. At each date on each Monte Carlo path the risk neutral hedges must be calculated, and each of those also require their own, nested, Monte Carlo simulation. The computational complexity means that insurers often hold more reserve than they need to, and potentially realize a lower return on capital.

Using deep hedging as an alternative

Deep hedging is an exciting new machine learning technique that uses a neural network to calculate hedge notionals, replacing traditional risk neutral pricing. The neural network is trained to give the best distribution of possible post-hedging profit/loss outcomes by minimizing the expected shortfall. The reserve held against the variable annuity book is the same expected shortfall, so deep hedging gives you a hedging strategy that minimizes reserves.

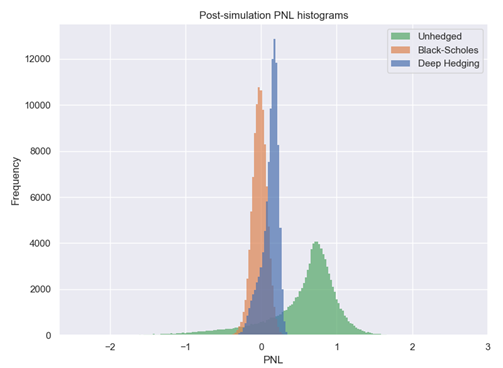

Here’s a chart showing profit/loss distribution over the life of a variable annuity portfolio, in three cases. Green (“Unhedged”) shows the distribution if there are no hedges included: that is, the profit and loss of the variable annuity issuance by itself. Orange (“Black-Scholes”) shows the distribution when hedges are included, calculated using traditional risk neutral pricing. And blue (“Deep Hedging”) shows the distribution when the hedging strategy is generated by the deep hedger, which has both a smaller expected shortfall than either of the other two distributions (realizing a smaller reserve for the insurer to hold) and a higher average profit than with risk neutral hedging.

The hedging strategy from the deep hedger is materially different to what you get from risk neutral pricing. The deep hedger tends to underhedge, taking some extra risk but also realizing some positive return because equity prices tend to increase over time. And this results in better outcomes and a smaller reserve.

To hedge or not to hedge?

Insurers have an option when calculating the reserve they hold against their variable annuity liabilities: they can include a rules-based hedging program in the reserve calculation, or assume no hedging. There are two incentives for them to not include a hedging program: the calculation can be computationally very expensive, because of the nested Monte Carlo simulation described above; and the reserve might actually be smaller if they do not include hedges.

That second point is a bit confusing, but is a result of equity prices tending to increase with time. Since issuing variable annuities makes the issuer long equities, being unhedged on average shifts the profit and loss distribution to the right. You can see that in the chart above: the average of the green (unhedged) distribution is much more positive than the other two.

This choice of “hedge or don’t hedge”, however, is a choice an insurer is forced to make only if they use risk neutral pricing to calculate hedges. The deep hedging technique finds a balance between those two extremes, suggesting a hedging strategy that tilts toward underhedging as average equity returns and variable annuity tenors increase.

Plus, deep hedging avoids the computational complexity of nested Monte Carlo simulations: calculating hedge ratios requires a neural network output, which is much faster than running a Monte Carlo simulation.

Deploying deep hedging in production

Implementing a robust deep hedging strategy requires several data and compute elements. First is the underlying actuarial and market data to build the analytics and run the scenarios. Second is the derivative analytics for the desired hedge pricing. Third, you need modern machine learning tools that can efficiently and effectively execute the calculations and build a neural network. Fourth is a significant compute grid that can run through the simulations in a reasonable time and cost, usually rented from a cloud provider so that you only pay for what you need. Finally, effective visualization and reporting tools analyze the results and present them to finance and management teams.

Improving return on equity

Deep hedging allows life insurers to hold smaller reserves against existing variable annuity portfolios, attain higher returns on equity, and lets them apply more efficient hedges than risk neutral pricing techniques can calculate. This technique also avoids the nested calculations problem that makes risk neutral hedges computationally infeasible for most organizations. Beacon’s integrated and enterprise-scale data and analytics platform includes all of the necessary elements to test and deploy new techniques like deep hedging that can materially improve your firm’s return on equity.

For more details on deep hedging and Beacon, you can watch our webinar or download the whitepaper. Or contact us to learn how Beacon Platform can help you transform your business.